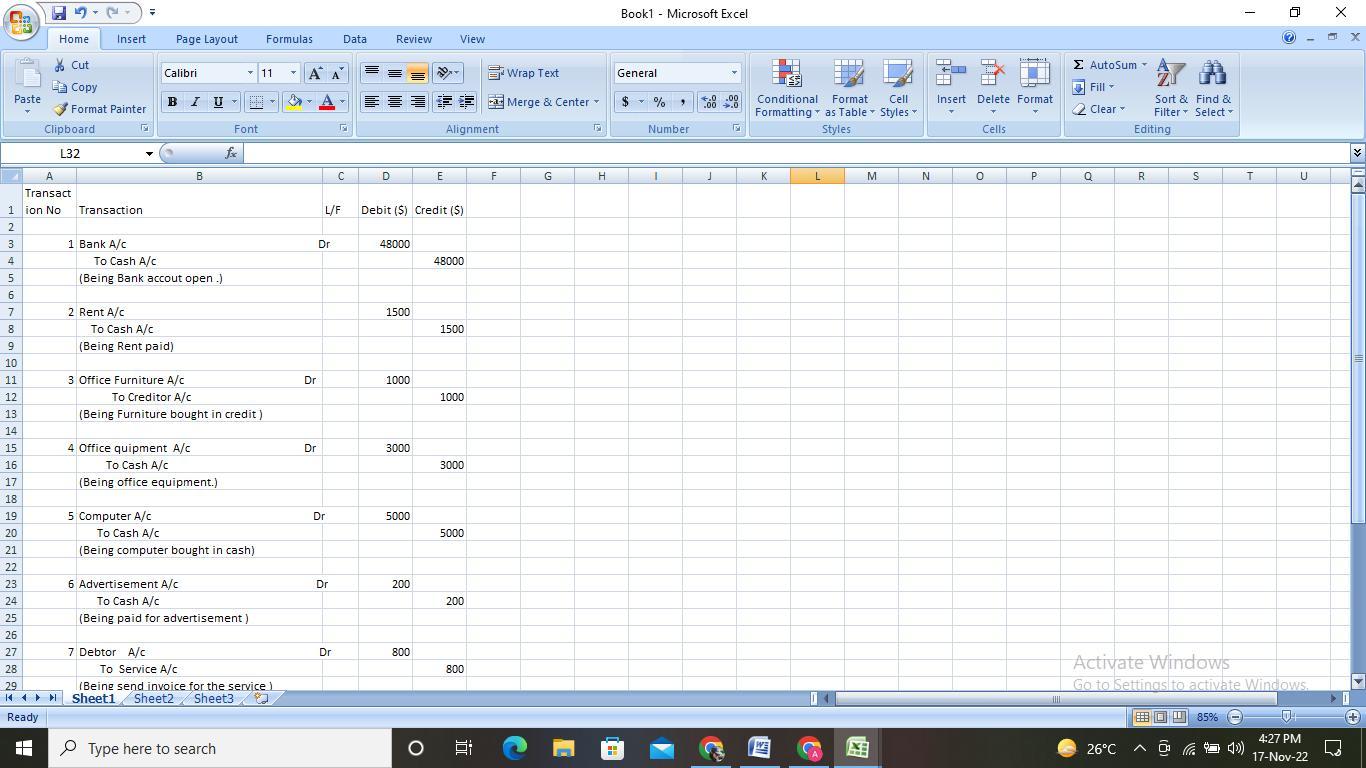

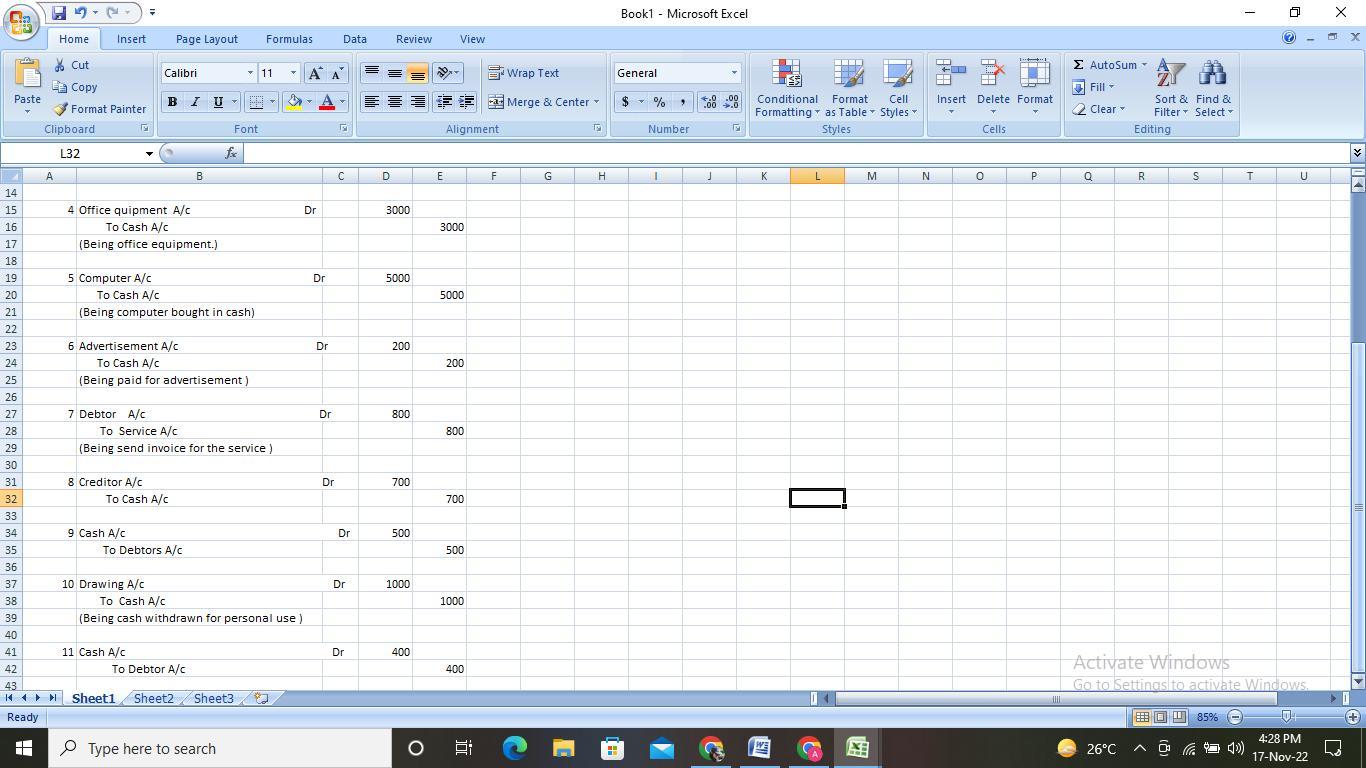

Please complete the spreadsheet template:

Trans no. Transaction

1. Pamela Wong, the owner, opened a checking account for the business by depositing $48,000 of her personal funds.

2. Paid the monthly rent of $1,500.

3. Bought office furniture on account for $1,000.

4. Pamela Wong invested $3,000 of office equipment in the business.

5. Paid cash for a new computer for the business, $5,000.

6. Paid for an advertisement in the local newspaper, $200.

7. Completed graphic desktop publishing services for a client and sent a bill for $800.

8. Paid $700 on account for the office furniture bought earlier.

9. Received $500 on account from a client.

10. Pamela Wong withdrew $1,000 for personal use.

11. Received $400 cash for desktop publishing services completed for a client.

Answers

Answer:

I used an excel spreadsheet sine there is not enough room here.

Explanation:

Excel templates make it simpler to create a spreadsheet with a polished appearance by including all of the following, with the exception of Data.

What is Excel Sheet ?To eliminate the necessity for the user to generate those designs from scratch, templates are made to specify the fundamental structure of each document that is repeated.

A template typically includes formatting and pre-defined formulas. However, it won't include any data as the template's goal is to have a consistent structure but allow for variable values so that it can respond appropriately to the data.

Formatting and pre-made formulas are frequently included in templates. Although the template aims to have a consistent structure and allow for variable values so that it can react appropriately to the data, it won't contain any data.

Any template will therefore include design but not data. We are able to make a new one, modify an existing template, or utilize the default template.

Learn more about Templates here

https://brainly.com/question/13270285

# SPJ 5

Related Questions

Mr Store who runs his photocopy business working 8 hours per day process 100 scripts. He estimates his labour cost to be € 9 per hour. Also he has estimated that the total material cost for each script is approximately € 2; while the daily expenses are €28. Calculate the multifactor productivity. In an effort to increase the rate of the photocopy process to 150 scripts, he decides to change the quality of ink thus raising the mate- rial cost to € 2.5 per day. Is the new productivity better than before? If Mr Store would like to increase the photocopy process to 150 scripts without sacrificing the initial multifactor productivity, by what amount has the material costs to be increased?

Answers

Answer:

A) 0.33 scripts per euro

B) The new productivity is worse than the old productivity

C) 0.333 euros per script

Explanation:

number of hours worked per day = 8

number of scripts processed per day = 100

Labor cost per hour = 9 euros

Total labor cost per day = 9 * 8 = 72 euros

material cost per script = 2 euros

Total material cost per day = 2 * 100 = 200 euros

daily expenses = 28 euros

A) Calculate the multifactor productivity

= output / Total cost

Total cost = ( 72 + 200 + 28 ) = 300

= 100 / 300

= 0.33 scripts per euro

B ) compare the old and new productivity

Old productivity = 0.33 scripts / euro

new multifactor productivity

= output / Total cost

Total cost = (8*9)+(150*2.5)+28 = 475

= 150 / 475

= 0.3158 scripts per euro

hence the new productivity is worse than the old productivity

C ) using the initial multifactor productivity of 0.333

calculate the target total cost = output / multifactor of productivity

= 150/0.333

= 450 euros

hence Material cost = (450 - 8*9-28)/150

= 2.33 euro per script

So, the material cost will be increased by = 2.33 euros - 2

euros

= 0.333 euros per script

The McMahon Construction Company builds bridges. In September and October 20XX, the company worked on a bridge covering the Kleinfeld River in Northern Montana. The McMahon Company has two departments, the Precast Department and the Construction Department. The Precast Department is responsible for building structural elements of bridges in temporary locations (plants) located near the construction sites. The Construction Department operates at the bridge site and they are responsible for assembling the precast structural elements. The estimated costs for Kleinfeld River Bridge for the Precast Department were $ 1,750,000 for direct materials, $ 240,000 for direct labor, and $300,000 for overhead. The estimated costs for the Construction Department regarding the Kleinfeld River Bridge were $ 400,000 for direct materials, $ 180,000 for direct labor, and $ 260,000 for overhead. Overhead is applied on the last day of the month. The Overhead application rate for the Precast Department is $ 30 per direct labor hour. The Overhead application for the Construction Department is 150 percent of direct labor cost.

Transactions for September

Sept 1- Purchased $ 1,170,000 of material on account for the Precast Department to start the building of structural elements. All of the material was issued to production, of the issuance amount, $ 720,000 is considered direct material.

Sept 4- Installed utilities at bridge site at a total cost of $30,000. The amount will be paid later in the month. (Transaction applies to Construction Department)

Sept 6-Paid rent for the temporary construction site housing the Precast Department, $ 7,200.

Sept 15- Completed the bridge support pillars by the Precast Department and transfer everything to the construction site.

Sept 19- Paid machine rental expense of $ 65,000 incurred by the Construction Department for clearing the bridge site and digging the foundations for bridge supports.

Sept 23- Purchased additional materials costing $1,510,000 on account.

Sept 30-The company paid the bills for the Precast Department: utilities, $ 7,200; direct labor, $50,000; insurance, $ 6,700, indirect labor, $ 8,200. Departmental depreciation was recorded, $21,500.

Sept 30-The company paid the bills for the Construction Department: utilities, $ 2,600; direct labor, $19,500; indirect labor, $6,100; and insurance, $ 2,500. Department depreciation was recorded on equipment, $ 9,450. Sept 30- Issued a check to pay for the material purchased on Sept 1 and Sept 23. Sept 30-Applied overhead to production in each department; 6,400 machine hours were worked in the Precast Department for September. Note: Direct Labor Costs for the Construction Department were $19,500.

Transactions for October

Oct 1- Transferred additional structural elements from the Precast Department to the construction site. The construction department incurred an expense of $ 7,000 to rent a crane.

Oct 4- Issued $1,010,000 of material to the Precast Department. Of this amount, $860,000 was considered direct.

Oct 7- Paid rent of cash of $ 7,500 in cash for the temporary site that is occupied by the Precast Department.

Oct 12-Issued $ 390,000 of material to the Construction Department. Of this amount, $ 220,000 was considered direct.

Oct 15-Transferred additional structural elements from the Precast Department to the construction site.

Oct 25-Transferred the final batch of structural elements from the Precast Department to the construction site.

Oct 29-Completed the bridge.

Oct 31-Paid the final bills for the month in the Precast Department: utilities, $ 14,000; direct labor, $120,000; insurance, $10,200; indirect labor, $18,300. Department depreciation was recorded, $21,500.

Oct 31-Paid the final bills for the month in the Construction Department: utilities, $ 5,300; direct labor, $144,500; indirect labor, $19,200; and insurance, $ 7,400. Depreciation was recorded on equipment was $9,450.

Oct 31-Applied overhead in each department. The precast department recorded 4,120 machine hours in October.

Oct 31-Billed the state of Montana for the completed bridge at the contract price of $3,850,000.

Oct 31-Please record the cost of the completed jobs to Finished Goods Inventory.

Required:

Journalize the entries for the preceding transactions. For purposes of this case study it is not necessary to transfer direct material and direct labor from one department to another.

Answers

Answer:

The McMahon Construction Company

Journal Entries:

Sept. 1:

Debit Precast Direct Materials Inventory $1,170,000

Credit Accounts Payable $1,170,000

To record the purchase of materials on account for Precast.

Debit Work in Process-Precast $720,000

Debit Manufacturing Overhead (Precast Dept.) $450,000

Credit Precast Direct Materials Inventory $1,170,000

Sept. 4:

Debit Manufacturing Overhead (Construction Dept.):

Utilities Expense $30,000

Credit Utilities Payable $30,000

To recorde utilities installed at bridge site.

Sept 6:

Debit Manufacturing Overhead (Precast Dept.):

Rent Expense $7,200

Credit Cash Account $7,200

To record the payment of rent for the temporary construction site.

Sept. 15:

No journal entries.

Sept 19:

Debit Manufacturing Overhead (Construction Dept.):

Machine Rental Expense $65,000

Credit Cash Account $65,000

To record the payment of machine rental expense

Sept. 23:

Debit Direct Materials Inventory $1,510,000

Credit Accounts Payable $1,510,000

To record the purchase of additional materials on account.

Sept. 30:

Debit:

Utilities Payable-Precast Dept $7,200

Direct labor -Precast Dept. $50,000

Debit Manufacturing Overhead (Precast Dept.):

Insurance Expense- Precast $6,700

Indirect labor $8,200

Credit Cash Account $72,100

Debit Manufacturing Overhead (Precast Dept.):

Depreciation Expense$21,500

Credit Accumulated Depreciation - Precast Dept $21,500

To record the depreciation expense for the month.

Sept. 30:

Debit Work in Process: Direct labor $19,500

Debit Manufacturing Overhead (Construction Dept.):

Utilities Expense t $2,600

Indirect labor $6,100

Insurance Expense $2,500

Credit Cash Account $30,700

Debit Manufacturing Overhead (Construction Dept.):

Depreciation Expense $9,450

Credit Accumulated Depreciation - Construction Dept $9,450

To record the depreciation expense for the month.

Debit Accounts Payable $2,680,000

Credit Cash Account $2,689,000

To record the payment on account by a check issued.

Debit Work in Process (Precast) $192,000

Credit Manufacturing Overhead (Precast) $192,000

To apply overhead to production in Precast Dept.

Debit Work in Process (Construction Dept.) $29,250

Credit Manufacturing Overhead (Construction Dept.) $9,250

To apply overhead to production in the construction department.

October:

Oct. 1:

Debit Manufacturing Overhead (Construction Dept.) $7,000

Credit Cash Account $7,000

To record the cost of rental a crane.

Oct. 4:

Debit Raw Materials Inventory (Precast) $860,000

Debit Manufacturing Overhead (Precast) $150,000

Credit Raw Materials Inventory.

Oct. 7:

Debit Manufacturing Overhead (Precast Dept.):

Rent Expense $7,500

Credit Cash Account $7,500

To record the payment of rent for cash.

Oct. 12:

Debit Work in Process (Construction Dept.) $220,000

Debit Manufacturing overhead-170,000

Credit Raw Materials $390,000

To record the issue of materials to the construction dept.

Oct. 15:

No Journal Entries required

Oct. 25:

No Journal Entries required

Oct. 29:

No. Journal Required

Oct. 31:

Debit:

Work in Process (Direct labor) $120,000

Manufacturing Overhead (Precast):

Utilities $14,000

Insurance $10,200

Indirect labor $18,300

Credit Cash Account $162,500

Oct. 31:

Debit Manufacturing Overhead (Precast Dept.):

Depreciation Expense$21,500

Credit Accumulated Depreciation - Precast Dept $21,500

To record the depreciation expense for the month.

Oct 31:

Debit Work in Process: Direct labor $144,500

Debit Manufacturing (Construction Dept.):

Utilities Expense t $5,300

Indirect labor $19,200

Insurance Expense $7,400

Credit Cash Account $176,400

To record the payment of cash for the expense

Debit Manufacturing Overhead (Construction Dept.):

Depreciation Expense $9,450

Credit Accumulated Depreciation - Construction Dept $9,450

To record the depreciation expense for the month.

Debit Work in Process (Precast) $123,600

Credit Manufacturing Overhead (Precast) $123,600

To apply overhead to production in Precast Dept.

Debit Work in Process (Construction Dept.) $216,750

Credit Manufacturing Overhead (Construction Dept.) $216,750

To apply overhead to production in the construction department.

Debit Accounts Receivable (State of Montana) $3,850,000

Credit Service Revenue $3,850,000

To record the billing of the state for the completed bridge.

Debit Finished Goods Inventory $1,835,600

Credit Work in Process $1,835,600

To record the cost of the completed jobs.

Explanation:

a) Data:

Estimated costs for Kleinfeld River Bridge

Precast Construction

Department Department

Direct materials $ 1,750,000 $ 400,000

Direct labor 240,000 180,000

Overhead 300,000 260,000

Overhead application $30 per DMH 150% DL

Machine hours worked 6,400 MH $19,500

Work in Process:

Materials $720,000

Direct labor (precast) 50,000

Direct labor (construction) 19,500

Overhead applied 192,000

Overhead applied 29,250

Materials 220,000

Direct labor 120,000

Direct labor 144,500

Overhead applied 123,600

Overhead applied 216,750

Total cost $1,835,600

Carol really doesn't like her new boss and is not happy with the new tasks she's been assigned and the long hours she's been working. Still, she truly believes in what the company is trying to accomplish. Carol has Question 9 options: 1) low organizational commitment. 2) poor job enrichment. 3) poor job performance. 4) low job satisfaction. 5) low job involvement.

Answers

Answer:

4)Low job satisfaction

Explanation:

From the question, we are informed that Carol really doesn't like her new boss and is not happy with the new tasks she's been assigned and the long hours she's been working. But she still truly believes in what the company is trying to accomplish.

In this case , Carol has Low job satisfaction.

Whenever an employee job

has satisfaction, he/she will be motivated, it always result to efficiency in the part of employees, they ten to work harder for acheiving the goal of the organization which in turn result to good overall performance of the organization. But in the situation whereby an employee has

Low job satisfaction, the reverse is the case, he/she will not be happy with task given to him/her, no motivation.

Factors that improve Low job satisfaction are;

✓Assuring job security for employee

✓Job benefits

✓Good relationship between employee and employer.

Your neighbor is asking you to invest in a venture that will double your money in 7 year(s). Compute the annual rate of return that he is promising you?

Answers

Answer: 10.3%

Explanation:

The Rule of 72 is useful here. The rule of 72 can be used to calculate the amount of time it would take to double an investment by dividing 72 by the interest rate.

As we already have the number of years the formula is;

7 = 72/i

i = 72/7

i = 10.3%

Suppose the classical linear model assumptions hold, and the population model for log(wage) is given by:

Answers

Answer:

Throughout the clarification segment down, the definition including its concern is explained.

Explanation:

The query presented seems to be incomplete. Please notice the full issue attachment below.

The classical model relies on either the calculation as well as assumption of "finite sample," suggesting that perhaps the amount of measurements "n" is defined.Present work does not affect salary seems to be:

⇒ H₀ : B₃ = 0

One side of the alterbate theory would be that ceteris paribus, duration at current employment seems to harm incomes.It is possible to state everything as:

⇒ H₁ : B₃<0

Making Podcasts and Wikis Work for BusinessPodcasts and wikis are part of Web 2.0, which allows users of the web to create content. Prudent business use of Web 2.0 applications can help businesses build and maintain their reputations online. Understanding how to use Web 2.0 communication tools will be important when you are on the job.Businesses have embraced podcasting to broadcast (confidential/ legal/ repetitive?) information that doesn’t require interaction. For example, some companies use podcasts to broadcast HR policies that can be accessed on demand. What function can companies improve by using wikis for collaboration?A. Communication with investors.B. Project management.

C. Customer interaction.

Consider the scenario:You work on the marketing team for a software development company. You have sales representatives in different locations around the globe. When a product update is released, your team holds teleconferences to demo new features. Due to time differences, these demos are difficult to schedule and usually require multiple demo sessions to accommodate different geographic regions. You want to streamline the new product demos and decide to recommend an electronic communication tool to help facilitate this. Which electronic communication tool would you recommend?A. A podcast.B. A wiki.C. An e-mail.

Answers

Answer:

(a) Businesses have adopted podcasting to communicate static material that doesn't need contact.

(b) Project management.

(c) A podcast

A further explanation is given below.

Explanation:

(a)

Podcasts should never be used to exchange legal or sensitive information because certain persons even within the company should readily determine it.(b)

Wikis could also be used for a fully customizable ecosystem which would be appropriate again for software engineering, as it means helping to work collaboratively, facilitate constructive criticism, as well as a supermarket recommendation for various use.(c)

Many persons may use podcasts throughout the current time, which does never demand conversation, it may be used to supplement the expensive conversation methods used. Emails as well as wiki shouldn't be used throughout this circumstance because that necessitates visuals among others to have been used.The rate of return on the common stock of Flowers by Flo is expected to be 14 percent in a boom economy, 8 percent in a normal economy, and only 2 percent in a recessionary economy. The probabilities of these economic states are 20 percent for a boom, 70 percent for a normal economy, and 10 percent for a recession. What is the variance of the returns

Answers

Answer:

the variance is 0.001044

Explanation:

The computation of the variance of the returns is shown below:

But before that expected return to be determined

E(r) = Sum of (probabilities × expected return)

= 0.20 × .14 + 0.70 × 0.08 + 0.10 × 0.02

= 0.086

Now

variance = Sum of (individual return - mean return)^2

= 0.20 × (0.14 -0.086)^2 + 0.7 × (0.08 - 0.086)^2 + 0.10 × (0.02 - 0.086)^2

= 0.001044

hence the variance is 0.001044

Re-Tire produces bagged mulch made from recycled tires. Production involves shredding tires and packaging the pieces for sale in the bagging department. All direct materials enter in the first process. The following describes production operations for October.

Direct materials used $226,000

Direct labor used 30% in Shredding; 70% in Bagging. $112,000

Predetermined overhead rate (based on direct labor) 165 %

Transferred to Bagging $206,500

Transferred to finished goods $583,000

The company's revenue for the month totaled $470,000 from credit sales, and its cost of goods sold for the month is $240,000.

Required:

Prepare summary journal entries dated October 31 to record its October production activities for:

a. Direct materials usage

b. Direct labor incurred

c. Overhead applied

d. Goods transfer from Shredding to Bagging.

e. Goods transfer from Bagging to finished goods.

f. Credit sales

g. Cost of goods sold.

Answers

Answer:

a.

Work In Process : Direct Materials $226,000 (debit)

Raw Materials $226,000 (credit)

Direct Materials used in production

b.

Work In Process : Shredding $33,600 (debit)

Work In Process : Bagging $78,400 (debit)

Salaries Payable $112,000 (credit)

Direct labor incurred during production

c.

Work In Process : Shredding $55,440 (debit)

Work In Process : $129,360 Bagging

Overheads $184,800 (credit)

Overheads applied to production cost

d.

Work In Process : Bagging $206,500 (debit)

Work In Process : Shredding $206,500 (credit)

Manufacturing costs transferred from Shredding to Bagging

e.

Work In Process : Shredding $583,000 (debit)

Finished Goods $583,000 (credit)

Manufacturing Costs transfer from Bagging to finished goods

f.

Account Receivable $470,000 (debit)

Sales Revenue $470,000 (credit)

Credit Sales during the month

g.

Cost of Goods Sold $240,000 (debit)

Finished Goods $240,000 (credit)

Cost of Goods Sold during the month

Explanation:

See the Journal entries and their narrations prepared above

The following are a trial balance and several transactions that relate to Lewisville's Concert Hall Bond Fund:

Lewisville Debt Service Fund Concert Hall Bond Fund Trial Balance July 1, 2012

Cash $60,000

Investments 40,000

Restricted fund balance $100,000

$100,000 $100,000

The following transactions took place between July 1, 2012, and June 30, 2013:

1. The city council of Lewisville adopted the budget for the Concert Hall Bond Fund for the fiscal year. The estimated revenues totaled $100,000, the estimated other financing sources totaled $50,000, and the appropriations totaled $125,000.

2. The General Fund transferred $50,000 to the fund.

3. To provide additional resources to service the bond issue, a property tax was levied upon the citizens. The total levy was $100,000, of which $95,000 was expected to be collected.

4. Property taxes of $60,000 were collected.

5. Revenue received in cash from the investments totaled $1,000.

6. Property taxes of $30,000 were collected.

7. The fund liability of $37,500 for interest was recorded, and that amount of cash was transferred to the fiscal agent.

8. A fee of $500 was paid to the fiscal agent.

9. Investment revenue totaling $1,000 was received in cash.

10. The fund liabilities for interest in the amount of $37,500 and principal in the amount of $50,000 were recorded, and cash for the total amount was transferred to the fiscal agent.

11. Investment revenue of S500 was accrued. Use the preceding information to do the following:

a. Prepare all the journal entries necessary to record the preceding transactions for the Concert Hall Bond Fund.

b. Prepare a trial balance for the Concert Hall Bond Fund as of June 30, 2013.

c. Prepare a statement of revenues, expenditures, and changes in fund balance and a balance sheet for the Concert Hall Bond Fund (assume all fund balance is restricted).

d. Prepare closing entries for the Concert Hall Bond Fund

Answers

Answer:

a. Journal entries

1. Estimated revenues (Dr.) $100,000

Estimated other financing sources (Dr.) $50,000

Appropriations (Cr.) $125,000

Fund Balance Budget (Cr.) $25,000

2. Cash (Dr.) $50,000

General Fund Transfer (Cr.) $50,000

3. Property Tax receivable (Dr.) $100,000

Uncollectable Taxes (Cr.) $5,000

Collectable Property taxes revenue (Cr.) $95,000

4. Cash (Dr.) $60,000

Collectable property tax revenue (Cr.) $60,000

5. Cash (Dr.) $1,000

Revenue From Investments (Cr.) $1,000

6. Cash (Dr.) $30,000

Collectable property tax revenue (Cr.) $30,000

7. Interest expense (Dr.) $37,500

Interest Payable (Cr.) $37,500

8. Fiscal Agent fee (Dr.) $500

Cash (Cr.) $500

9. Cash (Dr.) $1,000

Investment Revenue (Cr.) $1,000

10. Interest Expense (Dr.) $37,500

Principal payment (Dr.) $50,000

[Fiscal Agent] Cash (Cr.) $87,500

11. Investment Revenue Receivable (Dr.) $500

Investment Revenue (Cr.) $500

Explanation:

b. Trial Balance

Particulars : Debit (Dr.) $ ; Credit (Cr.) $

Cash: 76,500 ; 0

Property Taxes receivable 10,000 ; 0

Allowance for uncollectable property 0 ; 5,000

Investments 40,000 ; 0

Investment revenue receivable 500 ; 0

Restricted fund balance 0 ; 100,000

Revenue - property taxes 0 ; 95,000

Revenue- Investments 0 ; 2,500

Transfer to general fund 0 ; 50,000

Interest Expense 75,000 ; 0

Bond principal 50,000 ; 0

Fiscal agent fees 500 ; 0

Estimated revenues 100,000 ; 0

Estimated other financing sources 50,000 ; 0

Appropriations 0 ; 125,000

Fund balance Budget 0 ; 25,000

A common step in the testing for accounts payable is to test subsequent disbursements for improper/proper inclusion/exclusion in year-end accounts payable CONCEPT REVIEW A common way to test accounts payable is to examine the check register after period end and make selections for testing. Items are selected and then examined for detail. A determination is then made to conclude whether the amount should have been a liability as of year-end and, if so, if it was recorded as such

1. When searching for unrecorded liabilities, the auditors consider transactions recorded__________year end.

2. Accounts payable __________can be mailed to vendors from whom substantial purchases have been made.

3. To gain overall assurance as to the reasonableness of accounts payable, the auditor may consider _________.

4. When auditors find unrecorded liabilities, before adjusting they must consider __________.

5 Auditiors need to consider_______ terms for determining ownership and whether a liability should be recorded.

Answers

Answer:

1. When searching for unrecorded liabilities, the auditors consider transactions recorded after year end.

Auditors consider transactions recorded after year end to determine if it was supposed to be recorded in the current period.

2. Accounts payable confirmation can be mailed to vendors from whom substantial purchases have been made.

As a way to keep a document trail, creditors from whom substantial goods were bought from can be mailed a confirmation.

3. To gain overall assurance as to the reasonableness of accounts payable, the auditor may consider ratios.

Ratios such as the Payables turnover can be used to evaluate the reasonableness of Accounts payable.

4. When auditors find unrecorded liabilities, before adjusting they must consider materiality.

They must consider if the adjustment is material or significant enough to record.

5 Auditiors need to consider shipping terms terms for determining ownership and whether a liability should be recorded.

Shipping terms need to be considered because they can tell who owns goods in transit and therefore if a liability is needed for them. Shipping terms such as FOB Shipping point mean that the business incurs the liability as soon as the seller ships the goods.

Ming Chen began a professional practice on June 1 and plans to prepare financial statements at the end of each month. During June, Ming Chen (the owner) completed these transactions. ok ht inces

a. Owner invested $60,000 cash in the company along with equipment that had a $26,000 market value in exchange for its common stock.

b. The company paid $2,700 cash forfrent of office space for the month.

c. The company purchased $14,000 of additional equipment on credit (payment due within 30 days).

d. The company completed work for a client and immediately collected the $2,600 cash earned.

e. The company completed work for a client and sent a bill for $7,700 to be received within 30 days.

f. The company purchased additional equipment for $5,100 cash.

g. The company paid an assistant $4,000 cash as wages for the month.

h. The company collected $4,300 cash as a partial payment for the amount owed by the client in transaction e.

i. The company paid $14,000 cash to settle the liability created in transaction c.

j. The company paid $1,100 cash in dividends to the owner (sole shareholder). ad time

Required: Enter the impact of each transaction on individual items of the accounting equation. (Enter decreases to account balances with a minus sign.)

Answers

Answer:

I used an excel spreadsheet because there is not enough room here.

Explanation:

Eye Deal Optometry leased vision-testing equipment from Insight Machines on January 1, 2021. Insight Machines manufactured the equipment at a cost of $350,000 and lists a cash selling price of $437,810. Appropriate adjusting entries are made quarterly.

Related Information:

Lease term 5 years (20 quarterly periods)

Quarterly lease payments $26,250 at Jan. 1, 2021, and at Mar. 31, June 30, Sept. 30, and Dec. 31 thereafter

Economic life of asset 5 years

Interest rate charged by the lessor 8%

Required:

a. Prepare appropriate entries for Eye Deal to record the arrangement at its beginning, January 1, 2021, and on March 31, 2021.

b. Prepare appropriate entries for Insight Machines to record the arrangement at its beginning, January 1, 2021, and on March 31, 2021.

Answers

Answer:

a. Prepare appropriate entries for Eye Deal to record the arrangement at its beginning, January 1, 2021, and on March 31, 2021.

we must first determine the present value of the lease payments:

PV of lease payments = quarterly payment x annuity factor

quarterly payment = $26,250PV annuity due factor, 2%, 20 periods = 16.67846PV of lease payment = $26,250 x 16.67846 = $437,809.56 ≈ $437,810

January 1, 2021, equipment leased from Insight Machines

Dr Right of use asset 437,810

Cr Lease payable 437,810

January 1, 2021, first lease payment

Dr Lease payable 26,250

Cr Cash 26,250

March 31, 2021, second lease payment

Dr Lease payable 18,019

Dr Interest expense 8,231

Cr Cash 26,250

interest expense = ($437,810 - $26,250) x 2% = $8,231

March 31, 2021, amortization expense

Dr Amortization expense 21,891

Cr Right of use asset 21,891

amortization expense = $437,810 / 20 = $21,891

b. Prepare appropriate entries for Insight Machines to record the arrangement at its beginning, January 1, 2021, and on March 31, 2021.

January 1, 2021, equipment leased to Eye Deal

Dr Lease receivable 437,810

Cr Lease revenue 437,810

Dr Cost of goods sold 350,000

Cr Equipment 350,000

January 1, 2021, first lease payment

Dr Cash 26,250

Cr lease receivable 26,250

March 31, 2021, second lease payment

Dr Cash 26,250

Cr Lease receivable 18,019

Cr Interest revenue 8,231

Which of the following best defines "Isolationist.?

a. The concept that a whole can derive more value than the combination of the individual parts. A common expression in defining synergy is 1+1 = 3, or each piece derives more value that it would on its own.

b. Two or more systems that depend or support one another, often achieving mutual benefit.

c. The process of international integrating arising from the interchange of world views, products, ideas, and other aspects of culture.

d. The notion that we have certain rights and responsibilities towards each other by the mere fact of being human on Earth.

e. Pertaining to a national (or group) policy of non-interaction with other nations (or groups).

Answers

Answer:

e. Pertaining to a national (or group) policy of non-interaction with other nations (or groups).

Explanation:

Isolationist is a strategic approach pertaining to a national (or group) policy of non-interaction with other nations (or groups). This ultimately implies that, an isolationist refers to a country that has a diplomatic policy of non-interaction or avoiding to have any form of alliance with other countries.

Generally, countries choose to practice isolationism because they want to avoid foreign economic commitments, preserve her identity and culture, protect its territory, etc. Between 1641 to 1853, The Tokugawa shogunate of Japan adopted isolationism known as "Kaikin" which made it avoid contact or alliance with other countries. Also, in 1930 China was isolationist by banning all maritime shipping activities.

Deferral adjustments are needed when the business:

a. Pays cash after the expense has been incurred.

b. Unanswered pays cash before the expense has been incurred.

c. Unanswered receives cash after the revenue has been generated.

d. Unanswered receives cash before the revenue has been generated.

Answers

Answer:

The correct answers are the options B and D: Pays cash before the expense has been incurred. And receives cash before the revenue has been generated.

Explanation:

To begin with, in the accounting field the term of "Deferral Adjustments" refers to those that the accountant does when they postpone the report of it in the income statement until a later period, so that means that when an event happens they might decide to postpone the report of that particular transaction doing what it is called "defer". Moreover, the two most common cases when the accountants use this technique are the ones choosen from the options, the cases B and D.

Statement of Members' Equity, Admitting New Member The statement of members' equity for Bonanza, LLC, follows:

Bonanza, LLC Statement of Members' Equity For the Years Ended December 31, 20Y3 and 20Y4

Idaho Properties, LLC, Member Equity Silver Streams, LLC, Member Equity Thomas Dunn, Member Equity Total Members' Equity

Members' equity, January 1, 20Y3 $273,000 $307,000 $580,000

Net income 57,000 133,000 190,000

Members' equity, December 31, 20Y3 $330,000 $440,000 $770,000

Dunn contribution, January 1, 20Y4 3,000 7,000 $220,000 230,000

Net income 62,500 137,500 50,000 250,000

Member withdrawals (32,000) (48,000) (40,000) (120,000)

Members' equity, December 31, 20Y4 $363,500 $536,500 $230,000 $1,130,000

Required:

a. What was the income-sharing ratio in 2016?

b. What was the income-sharing ratio in 2017?

c. How much cash did Thomas Dunn contribute to Bonanza, LLC, for his interest?

d. Why do the member equity accounts of Idaho Properties, LLC, and Silver Streams, LLC, have positive entries for Thomas Dunn’s contribution?

e. What percentage interest of Bonanza did Thomas Dunn acquire?

f. Why are withdrawals less than net income?

Answers

Answer:

a. Idaho Properties, LLC = $57000/190000 = 0.3 = 30%

Silver Streams, LLC = $133000/$190000 = 0.7 = 70%

income-sharing ratio = 3:7

b. Idaho Properties, LLC = 62500/250,000 = 0.25 = 25.0%

Silver Streams, LLC = 137500/250,000= 0.55 = 55.0%

Thomas Dunn = 50000/250,000 = 0.20 = 20.0%

income-sharing ratio = 25:55:20

c. Thomas Dunn’s provided a $230,000 cash contribution to the business. The amount credited to his member equity account is this amount less a $10,000 bonus paid to the other two members

d. The positive entries is due to bonus paid by Thomas Dunn

e. Thomas Dunn contribution $230,000

Idaho Properties, LLC, member equity $330,000

SilverStreams, LLC, member equity $440,000

Total Equity $1,000,000

Dunn Contribution/Total member equity = $220,000/$1,000,000 = 0.22 = 22%

In a large open economy , an investment tax credit raises the real interest rate, __________ the trade balance, and __________ net capital inflow.

Answers

Answer:

The correct approach will be "decreases, decreases."

Explanation:

The investment tax incentive helps corporations to exclude a portion of the expense including its investment towards taxes. This raises disposable income unintentionally. This increase in household inflation rate is contributing to something like an increase in the rate of trade.As either the significance of the domestic country's currency, export industries decreasing trend as well as imports rise, resulting throughout a decline throughout the terms of payment. The capital flows grow and indeed the outflow declines even as actual interest rates go up, the decline in net investment output.Which of the following is not a true statement about filing bankruptcy? a. Bankruptcy erases all of your debt. b. It is possible to rebuild your credit after filing bankruptcy. There are exemptions that alloW you to keep essentials. d. Bankruptcy stops aggressive action by creditors

Answers

The statement that is not true about bankruptcy is that Bankruptcy erases all of your debt. Option A is correct.

What is bankruptcy?Bankruptcy is a legal process or procedure that involves a person or business that is unable to repay its outstanding debts.

The bankruptcy methodology starts with a requisition or petition that is pointed by the debtor, which is most expected, or on behalf of creditors, and which is less common.

After filing bankruptcy, it is possible to rebuild credit after filing bankruptcy of a debtor, and there are certain waivers that allow maintaining the requirements.

Bankruptcy prevents assertive action by creditors, and it does not mean that it erases all of your debt.

Therefore, option A is correct.

Learn more about bankruptcy, refer to:

https://brainly.com/question/1142634

Answer:

A

Explanation:

Which of the following is not a true statement about filing bankruptcy?

a.

Bankruptcy erases all of your debt.

b.

It is possible to rebuild your credit after filing bankruptcy.

c.

There are exemptions that allow you to keep essentials.

d.

Bankruptcy stops aggressive action by creditors.

A

The Pritzker Music Pavilion in downtown Chicago is a technologically sophisticated and uniquely designed performing arts venue that hosts live concerts attended by over half a million patrons a year. A group of local organizers, led by a prominent local businesswoman, would like to use the pavilion for a concert to benefit a non-profit, national network of investors and environmental organizations working with companies and investors to address sustainability challenges such as global climate change. If the pavilion management agrees to host the concert, the organizers will donate all profits to Ceres (or absorb any losses).

Based on the following revenue and cost information, the organizers would like answers to several questions.

1. There are three sources of revenue for the concert:

2. Tickets will be sold for $15.50 each.

3. A large multinational corporation headquartered in Chicago will donate $2.00 per ticket sold.

4. Each concert attendee is expected to spend an average of $17.00 for parking, food, and merchandise.

5. On the expense side, there are also three components:

A popular national group has agreed to perform at the concert. Normally, the group demands a significant fixed fee to perform, but to reduce the risk for the organizers, the group has agreed to perform for $6.00 per ticket sold. The organizers will pay several companies to operate the parking, food, and merchandise concessions. They will pay $21,000 plus 15% of all parking, food, and merchandise revenue. The organizers will pay the pavilion $85,000 plus $7.00 per person attending to cover its operating expenses (production, maintenance, advertising, etc.)

Required:

a. What is the estimated contribution margin per ticket sold for the benefit concert?

b. What are the estimated total fixed costs for the benefit concert?

c. What is the estimated profit from the benefit concert if 10,500 tickets are sold?

d. How many tickets must be sold in order for concert profit to be $100,000?

e. Assuming a tax rate of 31% on profits from the concert, what must dollar ticket sales be in order for after-tax concert profits to be $100,000?

f. Assume that the organizers can negotiate the fixed payment for the pavilion's operating expenses. If the organizers expect to sell 10,500 tickets, how much can they afford to pay and still earn a profit of $100,000 (ignore taxes)?

Answers

Answer:

a. What is the estimated contribution margin per ticket sold for the benefit concert?

contribution margin per ticket = ($15.50 + $2 + $17) - ($6 + $2.55 + $7) = $34.50 - $15.55 = $18.95

b. What are the estimated total fixed costs for the benefit concert?

total fixed costs = $21,000 + $85,000 = $106,000

c. What is the estimated profit from the benefit concert if 10,500 tickets are sold?

estimated profit = (10,500 x $18.95) - $106,000 = $92,975

d. How many tickets must be sold in order for concert profit to be $100,000?

number of tickets sold = ($106,000 + $100,000) / $18.95 = 10,870.71 ≈ 10,871 tickets sold

e. Assuming a tax rate of 31% on profits from the concert, what must dollar ticket sales be in order for after-tax concert profits to be $100,000?

$100,000 / (1 - 31%) = $144,927.54

number of tickets sold = ($106,000 + $144,927.54) / $18.95 = 13,241.56 ≈ 13,241.56 tickets sold

f. Assume that the organizers can negotiate the fixed payment for the pavilion's operating expenses. If the organizers expect to sell 10,500 tickets, how much can they afford to pay and still earn a profit of $100,000 (ignore taxes)?

contribution margin increases to $18.95 + $7 = $25.95

10,500 = ($21,000 + $100,000 + ?) / $25.95

$272,475 = $121,000 + ?

? = $151,475

you can pay up to $151,475 in fixed expenses to the pavilion

You have a tax basis of ​$ and a useful life of five years and no salvage value. Provide a depreciation schedule ​(dk for k1​5) for ​% declining balance with switchover to straight line. Specify the year to switchover. Determine the depreciation amounts using the ​% declining balance and​ straight-line methods and BV amounts for each year

Answers

Answer:

the numbers are missing, so I will use another question as an example:

the asset's cost is $100,000useful life is 5 yearsno salvage value150% declining balancestraight line depreciation = $100,000 / 5 = $20,000

150% declining balance depreciation year 1 = 1.5 x $100,000 x 1/5 = $30,000, since it is higher than straight line we will use declining balance

book value at end of year 1 = $100,000 - $30,000 = $70,000

straight line deprecation = $70,000 / 4 = $17,500

150% declining balance depreciation year 2 = 1.5 x $70,000 x 1/5 = $28,000, since it is higher than straight line we will use declining balance

book value at end of year 2 = $70,000 - $28,000 = $42,000

straight line depreciation = $42,000 / 3 = $14,000, since it is higher than declining balance we will use straight line ⇒ switchover year

150% declining balance depreciation year 3 = 1.5 x $42,000 x 1/5 = $12,600

book value at end of year 3 = $42,000 - $14,000 = $28,000

depreciation year 4 = $14,000 (straight line)

book value at end of year 4 = $28,000 - $14,000 = $14,000

depreciation year 5 = $14,000 (straight line)

book value at end of year 5 = $14,000 - $14,000 = $0

Leach Inc. experienced the following events for the first two years of its operations:

Year 1:

Issued $10,000 of common stock for cash.

Provided $78,000 of services on account.

Provided $36,000 of services and received cash.

Collected $69,000 cash from accounts receivable.

Paid $38,000 of salaries expense for the year.

Adjusted the accounting records to reflect uncollectible accounts expense for the year.

Leach estimates that 5 percent of the ending accounts receivable balance will be uncollectible.

Closed the revenue account. Closed the expense account.

Year 2:

Wrote off an uncollectible account for $650.

Provided $88,000 of services on account.

Provided $32,000 of services and collected cash.

Collected $81,000 cash from accounts receivable.

Paid $65,000 of salaries expense for the year.

Adjusted the accounts to reflect uncollectible accounts expense for the year.

Leach estimates that 5 percent of the ending accounts receivable balance will be uncollectible.

Required

a. Record the Year 1 and Year 2 events in general journal form and post them to T-accounts.

b. Prepare the income statement, statement of changes in stockholders’ equity, balance sheet, and statement of cash flows for Year 1 and Year 2.

c. What is the net realizable value of the accounts receivable at Year 1 and Year 2?

Answers

Answer:

a.1) year 1

Issued $10,000 of common stock for cash.

Dr cash 10,000

Cr common stock 10,000

Provided $78,000 of services on account.

Dr accounts receivable 78,000

Cr service revenue 78,000

Provided $36,000 of services and received cash.

Dr cash 36,000

Cr service revenue 36,000

Collected $69,000 cash from accounts receivable.

Dr cash 69,000

Cr accounts receivable 69,000

Paid $38,000 of salaries expense for the year.

Dr wages expense 38,000

Cr cash 38,000

Adjusted the accounting records to reflect uncollectible accounts expense for the year. Leach estimates that 5 percent of the ending accounts receivable balance will be uncollectible.

Dr bad debt expense 450

Cr accounts receivable 450

Closed the revenue account. Closed the expense account.

Dr service revenue 114,000

Cr income summary 114,000

Dr income summary 38,450

Cr wages expense 38,000

Cr bad debt expense 450

Dr income summary 75,550

Cr retained earnings 75,550

b.1) income statement year 1Service revenue $114,000

Expenses:

Wages $38,000Bad debt $450 ($38,450)Net income $75,550

balance sheet year 1Assets:

Cash $77,000

Accounts receivable $8,550

total assets $85,550

Equity:

Common stock $10,000

Retained earnings $75,550

total equity $85,550

statement of cash flows year 1Cash flows form operating activities:

Net income $75,550

adjustments:

Increase in accounts receivable ($8,550)

net cash from operating activities $67,000

Cash flow from financing activities:

Common stocks issued $10,000

Net cash increase $77,000

beginning cash balance $0

Ending cash balance $87,000

a.2) Year 2:

Wrote off an uncollectible account for $650.

Dr bad debt expense 650

Cr accounts receivable 650

Provided $88,000 of services on account.

Dr accounts receivable 88,000

Cr service revenue 88,000

Provided $32,000 of services and collected cash.

Dr cash 32,000

Cr service revenue 32,000

Collected $81,000 cash from accounts receivable.

Dr cash 81,000

Cr accounts receivable 81,000

Paid $65,000 of salaries expense for the year.

Dr wages expense 65,000

Cr cash 65,000

Adjusted the accounts to reflect uncollectible accounts expense for the year. Leach estimates that 5 percent of the ending accounts receivable balance will be uncollectible.

Dr bad debt expense 745

Cr accounts receivable 745

b.2) income statement year 2Service revenue $120,000

Expenses:

Wages $65,000Bad debt $1,395 ($38,450)Net income $53,605

balance sheet year 2Assets:

Cash $125,000

Accounts receivable $14,155

total assets $139,155

Equity:

Common stock $10,000

Retained earnings $129,155

total equity $139,155

statement of cash flows year 2Cash flows form operating activities:

Net income $53,605

adjustments:

Increase in accounts receivable ($5,605)

net cash from operating activities $48,000

Net cash increase $48,000

beginning cash balance $77,000

Ending cash balance $125,000

c) net realizable value of accounts receivable at year 1 = $8,550

net realizable value of accounts receivable at year 2 = $14,155

a. Recording the Year 1 and Year events in general journal form and posting to T-accounts for Leach Inc. are as follows:

General JournalYear 1:

Debit Cash $10,000

Credit Common stock $10,000

Debit Accounts Receivable $78,000

Credit Service Revenue $78,000

Debit Cash $36,000

Credit Service Revenue $36,000

Debit Cash $69,000

Credit Accounts Receivable $69,000

Debit Salaries Expense $38,000

Credit Cash $38,000

Adjustment:

Debit Bad Debts Expense $450

Credit Uncollectible Allowance $450

Year 2:

Debit Accounts Receivable $650

Credit Uncollectible Allowance $650

Debit Accounts Receivable $88,000

Credit Service Revenue $88,000

Debit Cash $32,000

Credit Service Revenue $32,000

Debit Cash $81,000

Credit Accounts Receivable $81,000

Debit Salaries Expense $65,000

Credit Cash $65,000

Adjustment:

Debit Bad Debts Expense $968

Credit Uncollectible Allowance $968

T-accounts:Year 1:

Cash AccountCommon stock $10,000

Service Revenue $36,000

Accounts Receivable $69,000

Salaries Expense $38,000

Balance $77,000

Uncollectible AllowanceBad debts Expense $450

Common Stock

Cash account $10,000

Accounts Receivable

Service Revenue $78,000

Cash $69,000

Balance $9,000

Service RevenueAccounts Receivable $78,000

Cash $36,000

Income Summary $114,000

Salaries ExpenseCash $38,000

Income Summary $38,000

Bad Debts Expense

Uncollectible Allowance $450

Income Summary $450

Year 2:

Cash AccountBalance $77,000

Service Revenue $32,000

Accounts Receivable $81,000

Salaries Expense $65,000

Balance $125,000

Uncollectible AllowanceBalance $450

Accounts Receivable $650

Bad debts expense $968

Balance $768

Common StockBalance $10,000

Accounts Receivable

Balance $9,000

Service Revenue $88,000

Uncollectible allowance $650

Cash $81,000

Balance $15,350

Service RevenueAccounts Receivable $88,000

Cash $32,000

Income Summary $120,000

Salaries ExpenseCash $65,000

Income Summary $65,000

Bad Debts Expense

Uncollectible Allowance $968

Income Summary $968

b. The preparation of the income statement, statement of changes in stockholders' equity, balance sheet, and statement of cash flows for Year 1 and Year 2 are as follows:

Leach Inc.

Income Statements for Year 1 and Year 2:Year 1 Year 2

Service Revenue $114,000 $120,000

Salaries Expense 38,000 $65,000

Bad Debts Expense 450 38,450 968 65,968

Net income $75,550 $54,032

Leach Inc.

Statements of Changes in Stockholders' Equity for Year 1 and Year 2:Year 1 Year 2

Beginning balance $10,000 $85,550

Net income 75,550 54,032

Ending balance $85,550 $139,582

Leach Inc.

Balance Sheets at Year 1 and Year 2:Year 1 Year 2

Assets:

Cash $77,000 $125,000

Accounts Receivable 9,000 15,350

Uncollectible Allowance (450) (768)

Total assets $85,550 $139,582

Equity:

Ending balance $85,550 $139,582

Leach Inc.

Statements of Cash Flows for Year 1 and 2:Operating Activities: Year 1 Year 2

Net income $75,550 $54,032

Changes in working capital:

Accounts receivable (8,550) (6,032)

Operating cash flows $67,000 $48,000

Financing Activities:

Common Stock $10,000 $0

Increase in cash flows $77,000 $48,000

c. The net realizable value of the accounts receivable at Year 1 is $8,550 ($9,000 - $450) and Year 2 is $14,582 ($15,350 - $768).

Data Analysis:Year 1:

Cash $10,000 Common stock $10,000

Accounts Receivable $78,000 Service Revenue $78,000

Cash $36,000 Service Revenue $36,000

Cash $69,000 Accounts Receivable $69,000

Salaries Expense $38,000 Cash $38,000

Adjustment:

Bad Debts Expense $450 Uncollectible Allowance $450

Year 2:

Uncollectible Allowance $650 Accounts Receivable $650

Accounts Receivable $88,000 Service Revenue $88,000

Cash $32,000 Service Revenue $32,000

Cash $81,000 Accounts Receivable $81,000

Salaries Expense $65,000 Cash $65,000

Adjustment:

Bad Debts Expense $968 Uncollectible Allowance $968

= $968 ($650 + $768 - $450)

$768 ($15,350 x 5%)

Learn more about preparing financial statements at https://brainly.com/question/735261

Cramer Corporation formats operating cash flows using the indirect method. E:How do accounts receivable affect Cramer's cash flows from operating activities for 2018?

A. They increase cash provided by operating activities,

B. They don't because accounts receivable result from investing activities

C. They don't because accounts receivable result from financing activities.

D. They decrease cash provided by operating activities

Cramer's Income Statement for 2018

Sales revenue 170,000

Gain on sale of equipment 10,000 180.000

Cost of goods sold 110000

Depreciation 7500

Other operating expenses 27000 144500

Nel income 35500

The book value of equipment sold during 2018 was $22.000. 110,000 7.500 27.000 Done kerating activities for 2018? 1 Data Table Cash Accounts receivable

Cramer's Comparative Balance Sheets

December 31, 2018 and 2017

2018 2017

Cash 3,500 $ 2,000

Accounts payable 6,000 11,000

Accrued liabilities 8,000 7,000

Common stock 89,000 71,000

Retained earnings $ 106,500 $ 91,000

2018 2017

Accounts payable 7,000 $ 8,000

Accounts liabilities 9,000 1,000

Common stock 20,000 10000

Retained earnings 70500 72000

106,500 91,000

Answers

Answer: A. They increase cash provided by operating activities,

Explanation:

There is an error in the question. The Accounts Receivable are listed as Accounts Payable. Accounts receivable figures are $6,000 for 2018 and $11,000 for 2017.

The Accounts Receivable has therefore reduced in value from 2017 to 2018 by;

= 11,000 - 6,000

= $5,000

Seeing as Receivables have decreased, this means that some of those owing the business have paid their debt and so are no longer Accounts Receivable.

This payment of debt will increase the cash provided by operating activities.

A company has net working capital of $1,996. If all its current assets were liquidated, the company would receive $5,923. What are the company's current liabilities?

Answers

Answer:Current Liabilities= $3,927

Explanation:

Net working capital= Current assets-current liabilities

Current Liabilities = Current assets - Net working capital

= $5,923- $1,996

=$3,927

Current liabilities are short term liabilities , debt or obligation of a business which should be due within one year so as to be paid to creditors.

Cost of Goods Sold and Income Statement Schuch Company presents you with the following account balances taken from its December 31 adjusted trial balance:

Inventory, January 1 $40,000 Purchases returns $3,500

Selling expenses 35,000 Interest expense 4,000

Purchases 110,000 Sales discounts taken 2,000

Sales 280,000 Gain on sale of property (pretax) 7,000

General and administrative expenses 22,000 Freight-in 5,000

Additional data:

1. A physical count reveals an ending-inventory of $22,500 on December 31.

2. Twenty-five thousand shares of common stock have been outstanding the entire year.

3. The income tax rate is 30% on all items of income.

Required:

a. As a supporting document for Requirements 2 and 3, prepare a separate schedule for Schuch's cost of goods sold.

b. Prepare a 2013 multiple-step income statement.

c. Prepare a 2013 single-step income statement.

Answers

Answer:

Schuch Company

a) Schedule of Cost of Goods Sold

Inventory, January 1 $40,000

Purchases 110,000

Purchases returns -3,500

Freight-in 5,000

Cost of goods available for sale $151,500

less Inventory, December 31 22,500

Cost of goods sold $129,000

b) Multi-step Income Statement

For the year ended December 31, 2013:

Net Sales Revenue $278,000

Cost of Goods Sold 129,000

Gross profit $149,000

Expenses:

Selling expenses 35,000

General & admin exp. 22,000 57,000

Operating profit $92,000

Interest expense 4,000

Income after interest expense $88,000

Gain on sale of property (pretax) 7,000

Comprehensive income before tax $95,000

Income Tax (30%) 28,500

Net income $66,500

EPS = $2.66

c) Single-step Income Statement

For the year ended December 31, 2013:

Net Sales Revenue $278,000

Gain on sale of property (pretax) 7,000

Total revenue and gains $285,000

Cost of Goods Sold 129,000

Selling expenses 35,000

General & admin exp. 22,000

Interest expense 4,000

Total expenses $190,000

Income before taxes $95,000

Income Taxes (30%) 28,500

Net income $66,500

EPS = $2.66

Explanation:

a) Data and Calculations:

December 31 adjusted trial balance:

Inventory, January 1 $40,000

Purchases returns $3,500

Selling expenses 35,000

Interest expense 4,000

Purchases 110,000

Sales discounts taken 2,000

Sales 280,000

Gain on sale of property (pretax) 7,000

General and administrative expenses 22,000

Freight-in 5,000

Additional data:

Ending Inventory $22,500

Common Stock outstanding = 25,000

Income tax rate = 30%

Sales $ 280,000

Sales discounts taken 2,000

Net Sales Revenue $278,000

Producers of snack foods (such as candy bars or potato chips) are most likely to use a(n) _____________ distribution strategy for their products.

Answers

Answer:

A.intensive

Explanation:

Products such as chocolate bars and chips fit the classification of non-durable consumer goods, that is, those that are produced for immediate consumption.

Its characteristics involve meeting the needs of the final consumer periodically, generally they are low-cost products that need quick replacement to meet the high demand for these non-durable products.

Therefore, the best strategy for the distribution of non-durable products is the intensive strategy, making it available in different places with easy access to the consumer and with high replacement.

asper makes a $28,000, 90-day, 8.5% cash loan to Clayborn Co. The amount of interest that Jasper will collect on the loan is: (Use 360 days a year.)

Answers

Answer:

$595

Explanation:

The computation of the amount of interest is shown below:-

Amount of interest = Loan amount × Interest rate × Number of days ÷ Number of days in a year

= $28,000 × 8.5% × 90 ÷ 360

= $595

Therefore for computing the amount of interest we simply applied the above formula.

And the same is to be considered

The opportunity cost of making a component part in a factory with no excess capacity is the: (CMA adapted)

Answers

Answer:

Answer Choices

The opportunity cost of making a component part in a factory with no excess capacity is the

(A) Variable manufacturing cost of the component.

(B) Fixed manufacturing cost of the component.

(C) Cost of the production given up in order to manufacture the component.

(D) Net benefit given up from the best alternative use of the capacity.

Answer is D

Net benefit given up from the best alternative use of the capacity.

Explanation:

When we talk about opportunity cost, we simply look at the potential benefits a business, investor or person could miss when selecting a particular alternative over another. This is a major concept in economics.

If one is not careful, opportunity costs can be readily overlooked and when one tries to understand the missed opportunities in choosing one option over another, that individual would be able to make better decisions.

In both the United States and France, the demand for haircuts is given by QD=300−10P . However, in the United States, the supply is given by QS=−300+20P , while in France, the supply is given by QS=−33.33+6.67P .

Required:

a. What are the equilibrium prices and quantities of haircuts in the two countries?

b. What are the new equilibrium prices and quantities of haircuts in the two countries?

Answers

Answer:

a. P = 20 and Q = 100 in the United States; and also P = 20 and Q = 100 in France.

b. P = 23.33 and Q = 166.70 in the United States; and P = 26 and Q = 140 in France.

Explanation:

Note: The part b of the requirement is not complete. The entire question is therefore represented with the complete pat b before answering the question as follows:

In both the United States and France, the demand for haircuts is given by QD=300−10P . However, in the United States, the supply is given by QS=−300+20P , while in France, the supply is given by QS=−33.33+6.67P .

Required:

a. What are the equilibrium prices and quantities of haircuts in the two countries?

b. Suppose that the demand for haircuts in both countries increases by 100 units at each price, so that the new demand is QD = 400 - 10P. What are the new equilibrium prices and quantities of haircuts in the two countries?

The explanation to the answers is now provided as follows:

a. What are the equilibrium prices and quantities of haircuts in the two countries?

In economics, an equilibrium occurs at point where the quantities demanded is equal to the quantities supplied.

Let Q denotes equilibrium quantity and P denotes equilibrium price, the equilibrium prices and quantities of haircuts in the two countries can therefore be calculated as follows:

In the United States

QD =300 − 10P

QS= −300 + 20P

Since at equilibrium, QD = QS, we can therefore solve for P by equating the two equations above as follows:

300 - 10P = −300 + 20P

300 + 300 = 20P + 10P

600 = 30P

P = 600 / 30

P = 20

To obtain equilibrium quantity, we substitute P = 20 into any QD and QS since at equilibrium QD = QS. Using QD, we have:

Q = 300 – 10(20)

Q = 300 – 200

Q = 100

Therefore, P = 20 and Q = 100 in the United States.

In France

QD = 300 − 10P

QS= −33.33 + 6.67P

Since at equilibrium, QD = QS, we can therefore solve for P by equating the two equations above as follows:

300 - 10P = −33.33 + 6.67P

300 + 33.33 = 6.67P + 10P

333.33 = 16.67P

P = 333.33 / 16.67

P = 20

To obtain equilibrium quantity, we substitute P = 20 into any QD and QS since at equilibrium QD = QS. Using QD, we have:

Q = 300 – 10(20)

Q = 300 – 200

Q = 100

Therefore, P = 20 and Q = 100 also in France.

b. Suppose that the demand for haircuts in both countries increases by 100 units at each price, so that the new demand is QD = 400 - 10P. What are the new equilibrium prices and quantities of haircuts in the two countries?

In the United States

QD = 400 − 10P

QS= −300 + 20P

Since at equilibrium, QD = QS, we can therefore solve for P by equating the two equations above as follows:

400 - 10P = −300 + 20P

400 + 300 = 20P + 10P

700 = 30P

P = 700 / 30

P = 23.33

To obtain equilibrium quantity, we substitute P = 20 into any QD and QS since at equilibrium QD = QS. Using QD, we have:

Q = 400 – 10(23.33)

Q = 400 – 233.30

Q = 166.70

Therefore, P = 23.33 and Q = 166.70 in the United States.

In France

QD = 400 − 10P

QS= −33.33 + 6.67P

Since at equilibrium, QD = QS, we can therefore solve for P by equating the two equations above as follows:

400 - 10P = −33.33 + 6.67P

400 + 33.33 = 6.67P + 10P

433.33 = 16.67P

P = 433.33 / 16.67

P = 25.99 = 26

To obtain equilibrium quantity, we substitute P = 20 into any QD and QS since at equilibrium QD = QS. Using QD, we have:

Q = 400 – 10(26)

Q = 400 – 260

Q = 140

Therefore, P = 26 and Q = 140 in France.

Sparky Corporation uses the weighted-average method of process costing. The following information is available for February in its Molding Department:

Units:

Beginning Inventory: 30,000 units, 100% complete as to materials and 55% complete as to conversion.

Units started and completed: 120,000.

Units completed and transferred out: 150,000.

Ending Inventory: 32,500 units, 100% complete as to materials and 30% complete as to conversion.

Costs:

Costs in beginning Work in Process - Direct Materials: $48,000.

Costs in beginning Work in Process - Conversion: $53,850.

Costs incurred in February - Direct Materials: $328,050.

Costs incurred in February - Conversion: $604,150.

Required:

Calculate the cost per equivalent unit of materials.

Answers

Answer:

Cost per equivalent unit of material = $2.06

Explanation:

Total cost of material= Cost of material in beginning WIP + Cost of material incurred in February

= $48,000 + $328,050

= $376,050

Equivalent units = Number of units completed and transferred+ Ending inventory

= 150,000 units + 32,500 units

= 182,500 units

Cost per equivalent unit of material = Total cost of direct material / Equivalent units

= $376,050 / 182,500 units

= $2.06

on an annal basis, the first set of expenses is ____% of the second set of expenses. MAria spends 17 dollars on lottery tickets every week and spends

Answers

Completion Question:

On an annualbasis, the first set of expenses is _______% of the second set of expenses. Maria spends $17 on lottery tickets every week and spends $133 per month on food. On an annual basis, the money spent on lottery tickets is % of the money spent to buy food. (Round to the nearest percent asneeded.)

Answer:

Maria's Spending

On an annualbasis, the first set of expenses is ____55.39___% of the second set of expenses. Maria spends $17 on lottery tickets every week and spends $133 per month on food. On an annual basis, the money spent on lottery tickets is 55.39 % of the money spent to buy food.

Explanation:

Maria spends $17 on lottery tickets every week

Therefore, every 4-week month, she spends $68 ($17 * 4) on lottery tickets

Normally, a year = 52 weeks.

Annually, Maria spends $884 ($17 * 52) on lottery tickets

Also

Maria spends $133 per month on food.

Normally, a year = 12 months.

Annually, she spends $1,596 ($133 x 12) on food

Ratio of Lottery tickets to Food annually:

= $884 : $1,596

= $884/$1,596

= 55.39%

or

0.5539 : 1

b) What is done here is to convert to each cost to its annual equivalent. The cost of Lottery tickets was converted from per week basis to per annum. The cost of food was converted from per month basis to per annum. These conversions make the two variables comparable, since they have been reduced to similar standards of measurement.

Fields Company has two manufacturing departments, forming and painting. The company uses the weighted-average method of process costing. At the beginning of the month, the forming department has 36,000 units in inventory, 70% complete as to materials and 30% complete as to conversion costs. The beginning inventory cost of $82,100 consisted of $58,000 of direct materials costs and $24,100 of conversion costs.

During the month, the forming department started 520,000 units. At the end of the month, the forming department had 40,000 units in ending inventory, 85% complete as to materials and 35% complete as to conversion. Units completed in the forming department are transferred to the painting department. Cost information for the forming department is as follows:

Beginning work in process inventory $82,100

Direct materials added during the month 1,942,930

Conversion added during the month 1,359,730

1A. Calculate the equivalent units of production for the forming department.

1B. Calculate the costs per equivalent unit of production for the forming department.

1C. Using the weighted-average method, assign costs to the forming department’s output—specifically, its units transferred to painting and its ending work in process inventory.

Answers

Answer:

Please see attached detailed solution

Explanation:

1a. Direct material 550,000

Conversion 530,000

1b. Direct materials $3.64 per EUP

Conversion $2.61 per EUP

1c. Costs assigned to the forming department's output

• Total cost of ending work in process $160,300

• Total costs assigned $3,384,760

Please see attached detailed solution to the above questions and answers.